“The meanest reversion is the one that refuses to revert in a timely enough fashion.” – Josh Brown

I recently had a conversation with a friend who I play fantasy baseball with. We like to bounce ideas off each other, and occasionally commiserate when things don’t work out. My friend was bummed out because a few weeks ago he dropped Chris Taylor of the Dodgers. Since his move, Taylor has continued to rake. The rationale for cutting him was based largely on a sabermetric stat called BABIP.

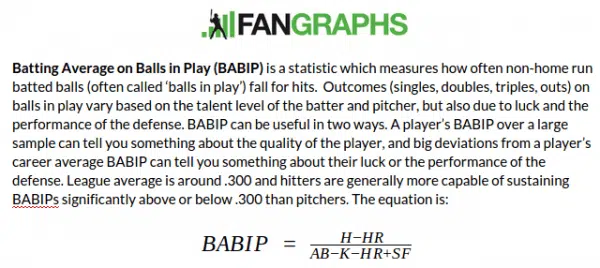

BABIP stands for “Batting Average on Balls in Play”. I’ll borrow a graphic from Fangraphs to define BABIP:

As the definition states, a .300 BABIP is about league average. This means roughly 30% of balls in play go for hits. We also know that the range for BABIP tends to stretch from .230 on the low end to .380 on the high end. Some players have BABIPs consistently better or worse than .300, but not many fall outside of that range.

Back to my friend’s decision. Chris Taylor currently maintains a BABIP of over .400. There have only been four instances in history where a player finished the season with a BABIP over .400. Knowing that, it seems like a near statistical certainty that Chris Taylor is due to regress, right? While Taylor will likely regress at some point, my friend learned the hard way that it doesn’t have to happen in a timely fashion. It doesn’t even have to happen this season for sure. We just know that it’s highly unlikely he continues at the rate he’s currently at.

Figuring out that something is due for mean reversion is a lot easier than figuring out when that reversion will actually occur. No matter how statistically certain it appears, using mean reversion as a timing tool can be a painful game.

This whole conversation with my friend about BABIP and mean reversion has eerie similarities to the ongoing discussion surrounding the US stock market’s CAPE ratio. For those who don’t know, the CAPE ratio looks at the average inflation-adjusted earnings from the previous ten years to determine how cheap or expensive US stocks are. It’s currently at expensive readings we’ve only seen a few other times in history.

Some investors get spooked by data like this and justifiably so. However, stocks have been relatively expensive for a few years now, so what to do with this data isn’t so black and white. It’s not as simple as: stocks are expensive, get out or stocks are cheap, get in. Unfortunately, that tends to be how people want to apply measures like CAPE.

If investors are searching for any one-off signal to make all-in, all-out calls with, they’re in for a lifetime of whipsaw and pain.

Meb Faber put it well when he wrote:

“I tell investors using valuation is a spectrum of future possibilities. While buying expensive markets generally will produce lower future returns, you will have positive outliers. The same for cheap markets, it’s usually a good idea but they can always get cheaper.”

Whether we’re talking about CAPE or BABIP, the real world presents countless factors (known and unknown) that can drive readings. For markets it may be things like GDP, market trend, inflation, interest rates, or corporate profits. For baseball players it could be pitching matchups, stadium effects, or the player’s health. Even statistically reliable indicators will never be fail-safe because we’ll never know precisely what factors are feeding into them or the degree to which they currently matter.

My advice is that if you’re banking on reversion occurring, just remember how mean it can be in the interim.

Further reading:

http://mebfaber.com/2014/08/22/everything-you-need-to-know-about-the-cape-ratio/