Stocks and bonds both had a volatile first quarter. This has many investors considering a peculiar question: Is there more risk in the stock or bond side of my balanced portfolio?

Based upon what’s occurred so far in 2022, this is a reasonable thing to wonder. Both the Bloomberg Aggregate Bond Index and the S&P 500 finished down for the first quarter, and (depending on how you get your particular stock-bond exposure) you may have lost more in bonds than stocks.

While stock market volatility is never fun, it is, at least, expected. Bonds, on the other hand, are typically valued for their stability, and especially their stability when stocks are falling, which is what makes the first quarter of 2022 surprising.

What’s happening with bonds?

In order to combat inflation, the Federal Reserve raised its benchmark interest rate for the first time since late 2018. They’ve also committed to raising rates as much as necessary to get inflation under control. When interest rates rise, bond prices fall. The bond market is pricing in the expectation of a hiking Federal Reserve, sending bond prices down, as a result.

Here are some questions we’ve been fielding related to bonds:

How bad is it for bonds?

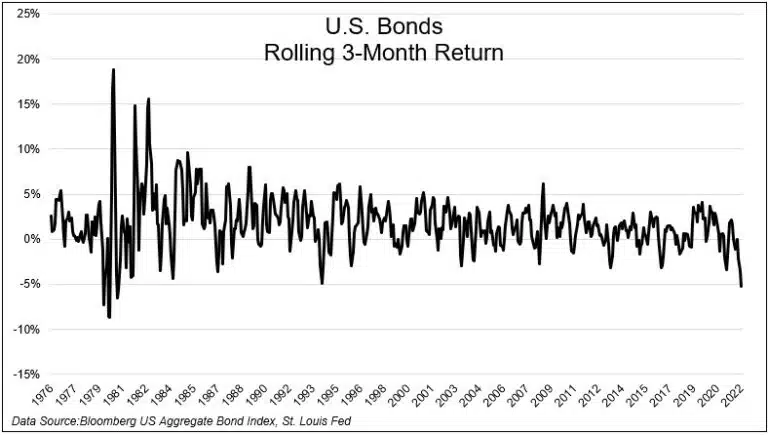

The most recent three month stretch for bonds is amongst the worst in history.

As evidenced by the chart below, the worst rolling three month periods for bonds have historically been between -5-10%. We’re there right now.

It’s important to remember that the sort of downside we’ve recently seen in bonds is still absolutely nothing compared to what stocks can do over a similar period of time – remember the -34% drop in the S&P 500 from February to March of 2020?

Bonds are absolutely not risk-free, but (even at their worst) they are far less volatile than stocks.

Will stocks and bonds continue to fall in lockstep?

Based upon history, it’s unlikely that stocks and bonds will continue to fall together.

In fact, according to Michael Batnick of Ritholtz Wealth Management, “the S&P 500 and the Bloomberg US Aggregate bond index have both declined for consecutive months just ten times since 1976. They’ve never both had negative returns for three straight months.”

This speaks to the complementary relationship that stocks and bonds bring a portfolio. One generally zigs while the other zags, and vice versa, which is what makes them good teammates.

Unfortunately, diversification doesn’t work 100% of the time. We see the recent results as more of an exception to the rule than a new normal.

Will bonds still diversify stocks in a rising rate environment?

While we should not expect bonds to do as well overall in a rising rate environment, they have historically still diversified stocks just the same. Cullen Roche of Discipline Funds took a look at bond returns during the rising rate environment from 1940-1980, and found that they still smoothed the ride for investors who couldn’t tolerate being 100% in stocks.

Should we sell our longer term bonds in favor of shorter term bonds?

When interest rates rise, longer term bonds suffer bigger losses than shorter term bonds (all else equal). But, even if we knew in advance the precise timing, length, and magnitude of the entire current Fed hiking cycle, we still might get this trade wrong.

For the last 10 years, there have been endless calls to hold shorter term bonds vs. longer term due to the risk of rising rates – see this from 2013 and this from 2018, for instance. Only until the last several months have these calls done anything beside cost investors money.

Trying to predict (and therefore time) the interest rate market is just as difficult as trying to time the stock market. The odds of doing so successfully (in a repeatable way) are slim to none.

We’d prefer to see investors match assets and liabilities in their portfolio with short term needs covered by short term bonds, intermediate term needs covered by a mix of intermediate term bonds and stocks, and long term needs covered by stocks. Rather than trying to predict interest rate movements, and their corresponding impact on bond investments, we invest the dollars according to when they’ll be needed.

What about holding cash instead of bonds altogether?

Given the current interest rate risk on bonds, that may seem wise in the short-term, but it is unlikely to be wise in the long-term. On a day-to-day (or even year-to-year basis), we cannot predict whether stocks, bonds, or cash will perform better. However, over longer periods of time, we believe that investors are compensated for the level of risk they choose to bear.

Considering that stocks are riskier than bonds, and bonds are riskier than cash, we expect investors holding money in bonds to do better than investors holding cash. While this has not been true over the last calendar quarter (or year), it has been reliably true over longer periods of time.

Assuming cash will outperform bonds over the long term is a low probability bet.

A final point about bonds:

It has been demonstrated that the best predictor of future bond returns is the starting yield. While short term losses stink, rising interest rates are the best possible thing we could hope for as long term bond investors.

In a rising rate environment, as bond funds reinvest proceeds from maturing individual bonds, the new bonds it purchases will have higher yields. This means larger interest payments to investors, and therefore better returns in the long run.

Unfortunately, as is always the case, the short-term pain is required in order to reap the long-term gain.