? 1:52 - Should I sell my stocks to cover expenses from an emergency room visit? 4:39 - Financial shocks 6:28 - Tax on the poor Here is the transcription for this video.

Mullooly Asset Show Episode 11

read more

? 1:52 - Should I sell my stocks to cover expenses from an emergency room visit? 4:39 - Financial shocks 6:28 - Tax on the poor Here is the transcription for this video.

Imagine that you and your family are about to take a cruise to the Caribbean. You'll be stopping in St. Lucia, Grenada, and St. Vincent and the Grenadines. You're excited for what should be an excellent trip, but upon boarding you find out that the ship is taking on...

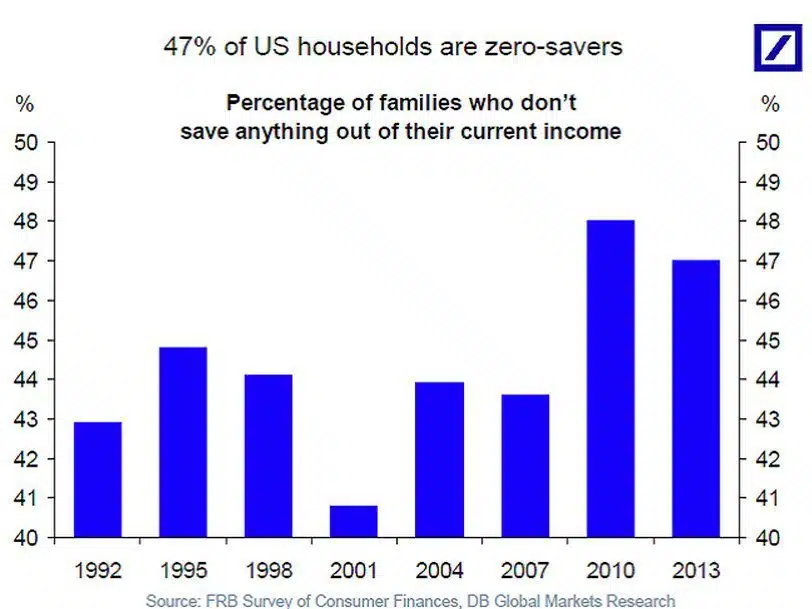

A recent chart from Deutsche Bank's Torsten Sløk shared on Business Insider shares a scary reality: 47% of US households don't save any part of their current income. Of course, as Anthony Isola put it on Twitter, "Making lemonade out of lemons, 53% save something!"....

The beginning of a new year presents an optimal time to set goals for yourself. Last week, Tom discussed financial New Year's resolutions on the weekly video. I recently read an excellent post from Kris Venne of Ritholtz Wealth Management regarding knowing your...

As 2014 comes to an end, we share some timely tips for those who intend to make financial New Year's resolutions. Tom has some words of wisdom that you should keep in mind: Don't play the stock market with the rent! He elaborates on the meaning of this in our weekly...

In August of this year, BlackRock did a survey of 4,000 Americans. One of the most interesting things they discovered was surprising to me. According to their survey: As was true in our 2013 survey, "cash remains king" with almost two-thirds (63%) of all savings and...

There are several reasons you need to have an emergency fund, and Tom discusses them in this video from Mullooly Asset Management. Many people also wonder how much money they should have in their emergency fund when creating one. This is a good question to ask your...

In this week's Mullooly Asset Management podcast, Tom and Brendan discuss a question they hear a lot. The question is, "How much money should be in my emergency fund?". Tom was inspired to talk about financial safety nets this week because of a New York Times article...