In my last post I covered the basics of the Roth IRA. However, figuring out Roth IRA contributions can be tricky due to the phaseout rule. In this post I will provide examples of how to calculate Roth IRA contributions for a single tax filer and a married couple filing jointly.

Single Filer

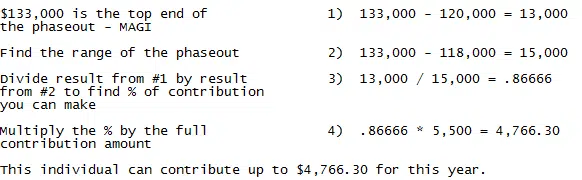

If a single individual makes less than $118,000 in 2017 he/she can contribute the full $5,500 to a Roth IRA. After the $118,000 threshold, a phase out begins. The phase out range is between $118,000 and $133,000. So if an individual has a modified adjusted gross income (MAGI) between $118,000 and $133,000 they can contribute a percentage of the full $5,500 contribution.

Below is an example of how a single individual would figure out how much he/she can contribute. Assume this individual has a MAGI of $120,000 in 2017:

If an individual has a MAGI of over $133,000 they will not be able to contribute to a Roth IRA that year.

Married Couple Filing Joint

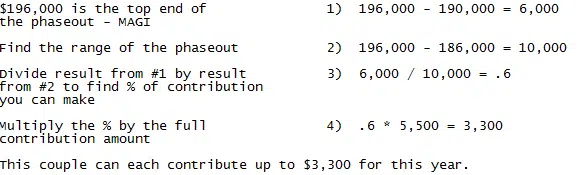

If a married couple has a MAGI under $186,000 they can both contribute up to the max of $5,500. Once past the MAGI of $186,000, a phaseout begins. The phase out range is between $186,000 and $196,000. So if a married couple has a modified adjusted gross income between $186,000 and $196,000 they can contribute a percentage of the $5,500.

Below is an example of how a married couple would figure out how much they can contribute. Assume this couple has a MAGI of $190,000 in 2017:

If a married couple has a MAGI of over $196,000 they will not be able to contribute to a Roth IRA that year.

An individual needs to be careful when figuring out how much he/she can contribute to a Roth IRA. The IRS makes it very confusing for people to figure out how much they can contribute to retirement accounts.

There are more rules and nuances that individuals have to take into consideration when contributing to retirement accounts. This post was written to provide some of the basics that people should understand. More posts will be coming out in the future that focus in on specific IRA topics.