Over my lifetime, I’ve compiled a nice long list of movies that I deem my favorites (as I’m sure everyone else has as well). One of the movies on the list is ‘Back To The Future’. I particularly enjoy ‘Back To The Future pt. II’ when Biff takes the DeLorean time machine from the future with the sports almanac to give to ‘past Biff’, which ultimately makes him rich knowing all of the outcomes of every sports game.

Wouldn’t that be nice, as an investor, to know the outcome of every trade you make BEFORE you make it?

This week, I worked my way back to an article by Wes Gray from Alpha Architect called “Even God Would Get Fired as an Active Investor”. Gray published this particular post back in February of 2016, but the message is evergreen.

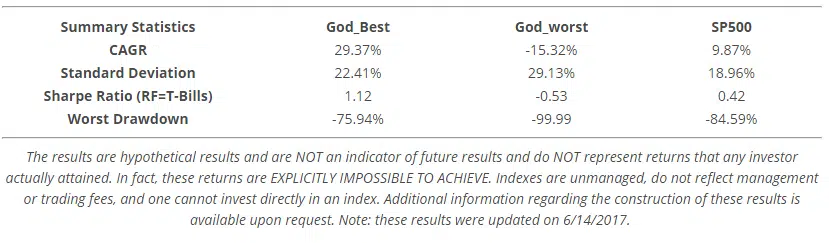

Gray talks about a hypothetical “portfolio” run by an all-knowing God that invests in the top decile of the top 500 stocks over a five-year period. Like Biff, God is able to pick the best performing stocks for a five-year period, and never lose. As Gray says “they are explicitly engaging in look-ahead bias”. The point that comes next really opened my eyes as an advisor.

Gray notes that while this “God portfolio” would compound at nearly 29% a year, the standard deviation and would be higher than that of the regular S&P 500, and the worst drawdown during that time would be -75.94%!

Even God Would Get Fired as an Active Investor

If there’s one thing I’ve learned in my years here at Mullooly Asset Management, it’s that people get very emotional about their money. Even the very best advisors would almost certainly get fired if they asked their clients to sit through a -75% drop in the account.

The post that triggered me to return to Gray’s piece was published this week by Nick Maggiulli over at Of Dollars and Data (if you haven’t check out Nick’s work, please do ASAP).

Maggiulli wrote about a conversation he had with the great Jim O’Shaughnessy. The ultimate moral of the conversation was a warning about how to properly use leverage, even in what seems to be a “can’t miss” situation (kind of like with Biff and his sports almanac).

The problem in Maggiulli’s situation (as you can read in full HERE), was that by trying to capitalize on a sure-thing by utilizing too much leverage, you would eventually wipe yourself out should that investment incur too many negative days in a row. By “wipe yourself out” I mean eventually get to a point where you have too little equity in the investment. It’s important to keep in mind that the force of leverage is great when it works on the upside, but it is equally as great when your investment turns negative as well.

As Maggiulli puts it,

even when we know the future with certainty, borrowing money isn’t a surefire solution to win big.

So if God would be fired as an active investor, knowing the future and borrowing money isn’t the solution, none of us have Biff Tannen’s Sports Almanac of Investing, how do investors stand a chance?

The point is that investing is inherently difficult for many people, and working with an advisor or planner would probably be their best bet.

Sure, there is a ridiculous amount of information on the internet today, and anybody is free to Google all of their questions. My caution to you, however, is this.

What kind of answers do people put on Google? In most cases it’s solutions to THEIR problems. Experiences THEY HAD. While there is a lot of ‘GOOD’ information on the internet, is it really the RIGHT information for you?

Working with an advisor, and creating a financial plan, is one way to help increase the odds of getting the right answers for your specific financial questions.

(PS – we talked about this very topic on this week’s episode of the Mullooly Asset Show! Watch it here!)

Your advisor can’t predict the future (and if he or she says otherwise, it’s a lie). What your advisor CAN do, however, is gather as much detail about your situation as possible and help nudge you in the right direction as you navigate through your financial life.

Kris Venne, Director of Wealth Management at Ritholtz Wealth Management, talked about this responsibility for advisors to use a financial plan as “behavioral nudges” in the right direction when making decisions during a conversation I had with him on an episode of the Living with Money podcast (check it out HERE).

It is the advisor’s job to make sure clients have a comprehensive financial plan to fall back on and use a ‘decision tree’ when tough financial curveballs are thrown their way.

So while there sadly is no Biff’s Sports Almanac of Investing, and the DeLorean is non-existent, there is still hope for investors out there. Use all of the information at your disposal, but remember that working with a professional who understands your specific situation can really increase your chances of making better choices.