Should You Be Managing Your Own Money in Retirement?

DIY: managing your own money in retirement works until it doesn’t. Here’s why that’s usually worth a second look.

Takeaways:

– As retirement nears, the money decisions pile up fast — and many are ones you’ve never had to make before.

– Withdrawal order, taxes, Social Security timing, Roth conversions, and RMDs all collide.

– A mistake hits harder at 65 than at 35 — there’s less time and no new income to recover from it.

– If you handle all the finances, having help in place protects your spouse if you’re suddenly not there to do it.

As mentioned in the video, here is some additional information for the do-it-yourself (DIY) investor and DIY Financial Planner.

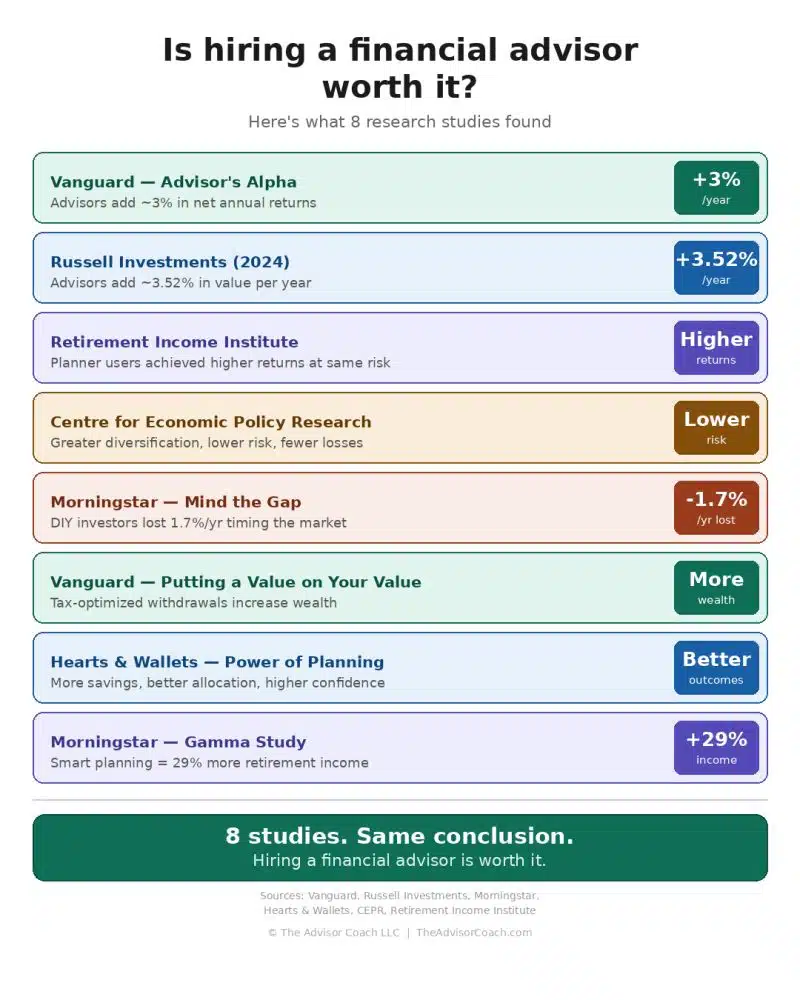

Is it “worth it” to hire a Financial Advisor? Here is some additional information provided by industry sources, not Mullooly Asset Management. Of course, your mileage may vary, your experience may very well be different from others – and nothing is ever guaranteed.

Information and graphic created by and reposted with permission from James Pollard. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided “as is” without any express or implied warranties. Past performance is not a guarantee of future results.

Should You Be Managing Your Own Money in Retirement – Links

Catch all our Mullooly Asset videos here

Subscribe to the Mullooly Asset YouTube Channel

Watch this episode (“Should You Be Managing Your Own Money In Retirement?”) on our YouTube Channel

Should You Be Managing Your Own Money in Retirement – Transcript

I hear this a lot from people who’ve managed their own investments for years and done a good job of it.

Somewhere in their late 50s or early 60s, a thought starts chipping away in their head,

“I, I wonder if I should get some help with this next part?”

If that’s where you are, here’s what I tell you.

I think you’re onto something.

As you get closer to retirement, the bigger decisions start piling up.

And they start piling up fast.

A lot of them are brand-new things, uh…….

….stuff you’ve never really had to deal with before.

For example, when the time comes…..

Which account should you be pulling money from first?

How do you pull money out without handing over too much to the IRS?

When do you turn on Social Security?

Do Roth conversions make sense for me?

And if Roth conversions make sense, well, how much do I do?

And what years do I take them?

And then before you know it, the required minimum distributions show up.

There’s a lot to it, and the rules are strict.

And there’s usually a bigger worry that’s running underneath all of that.

See, when you were 35 and you got something wrong, you literally had decades to work all of that out.

A bad year.

A panic sale when the market tanked.

You screwed up your taxes… somewhere along the way.

Time eventually bailed you out.

But at 65, that cushion is gone.

You’re not getting those years back.

You’re not adding new money to “gloss over” a mistake.

A wrong move could wind up leaving, uh, more than a skid mark.

Let’s just say (it could be) something more damaging today than it would’ve been, say, 20 or 25 years ago.

There is one more thing.

You’ve been the one that’s been handling all of this.

What happens if you’re not here?

Could your spouse actually take all of this over?

You know:

get into the accounts,

make the decisions,

know when to buy, when to sell,

what to do first in some of the things that we just mentioned…….

All while they’re grieving over your loss.

A lot of couples carry that question around for years.

They never bring it up at the dinner table.

They’d rather talk about who’s going to do the dishes tonight.

Getting some help now may be one of the kindest things you can do — for whoever you may leave behind.

So if this has been running through your mind, take that as a good sign.

The people who handle this stretch of their life well, tend to bring someone in early……..

while everything is still calm and everything is still on their terms.

There are folks who do the investing themselves – because they enjoy it.

They like the tinkering. They like the markets.

And that’s a perfectly good reason.

There’s also plenty written about “when it makes sense to bring in some help,”

And I’ve put some information below – if you want to read through that.

But if that nagging question keeps coming back to you, it’s usually worth listening to…….

Thanks for watching “DIY: Should you be managing your own money in retirement”